The Old Continent is seeking to regain competitiveness in a new global order marked by high energy costs, reduced technological importance, and a regulatory framework that is holding back its industrial momentum.

Europe is facing a harsh awakening from a scenario sustained for just over two decades by three pillars. Three pillars that can be summarized as the belief in a global order based on rules, agreements, and globalization; the support of cheap Russian energy; and the military protection of the United States. These fundamentals, however, have shifted, creating a new global paradigm that is forcing the Old Continent to reinvent itself, with the well-known Draghi Report as a possible guide and with Germany breaking its strict fiscal restraint.

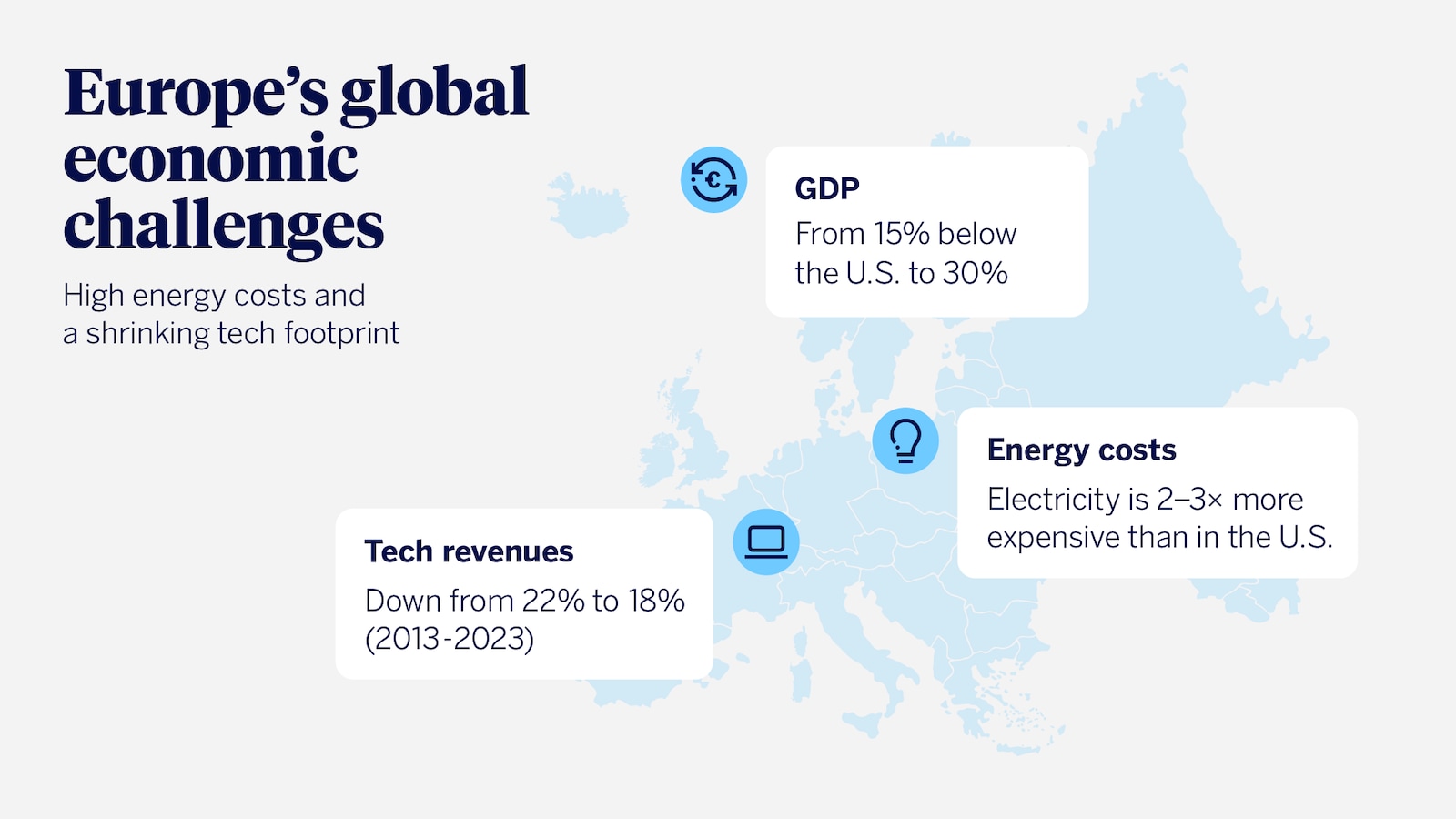

It is not only a matter of adapting to change, but also of survival. In terms of wealth, EU GDP was only 15% below that of the United States at the start of the century; today, it's 30% lower. Europe’s share of tech revenues between 2013 and 2023 has fallen from 22% to 18%, while the US share rose from 30% to 38%. The icing on the cake is that the industrial sector is facing electricity prices that are 2 to 3 times higher than those of its US counterpart.

Against this backdrop, Europe looks to the future with uncertainty, but also with solid foundations dating back to 1951. That was the year the European Coal and Steel Community (ECSC) was established, helping to develop a free market for coal and steel that laid the groundwork for a period of prosperity.

Back to the beginning: when Europe tore down walls

After two world wars, Europe came together from the second half of the 20th century onward. Thanks to those alliances and to a common, single market, the region’s GDP per capita rose from $8,500 in 1960 to $34,800 in 2024. This transformation created a level of social well-being never before seen in the region.

Notably, the well-known Draghi Report highlighted something that was one of the key drivers of that growth: regulation. In fact, the European Commission estimates that removing current barriers in the services sector could add another €450 billion annually to EU GDP.

For this reason, Aurelio García del Barrio, director of the Global MBA with a specialization in Finance at IEB, states that what Europe needs to regain competitiveness is “a common strategy on a continental scale for full energy integration, and a geopolitical vision, as opposed to excessive regulation, fragmentation, and the lack of a truly unified framework.”

That said, this expert points out that this is not a simple task, since “Europe regulates a market of 450 million people, and therefore a certain level of bureaucracy appears essential.” Even so, this does not change the fact that the main issue lies in excessive regulation: “all of this leads to slower project execution and penalizes startups and smaller companies.”

Tackling bureaucracy and diversifying trading partners

That return to the origins mentioned earlier points to two clear objectives: reducing bureaucracy and seeking new allies. Regarding the first point, in addition to what has already been said, one notable figure from the Draghi Report can be added. The former president of the European Central Bank (ECB) noted that, since 2019, the EU has approved 3,500 legislative acts and more than 2,000 regulations.

As for the second point, which has received less attention, it is worth highlighting the shift in global rules, with the United States no longer acting as such a close ally. Threats of tariffs from Donald Trump and decisions affecting global trade have led Europe to sign historic agreements with major markets such as India and Latin America.

For this reason, García del Barrio warns that Europe “must avoid dependence on a single alternative market and, of course, steer clear of the idea of replacing dependence on the United States with dependence on China.” For this reason, he highlights that the Old Continent should focus on India, ASEAN, and Africa to find new consumers; Africa, Australia, and Latin America for raw materials; Japan and South Korea for technology; and “the Persian Gulf for sovereign capital.”

Is there room to respond? Europe's hope

The problems and the past have been broadly outlined in this article. Aware of these threats, Europe is beginning to respond with a rearmament plan and an industrial plan, particularly in Germany. But before looking ahead, the IEB professor adds a caveat, noting that “Europe still faces a fragmented capital market and fiscal asymmetries between states, and therefore should have an effective capital market and permanent common fiscal instruments beyond extraordinary funds such as the Next Generation.”

In addition to this challenge, the objectives for coming years should focus on “achieving competitive energy, a strong industrial policy, simplifying regulation, and, lastly, independence in defense matters,” says Aurelio García del Barrio.

Looking at projections, PwC and Goldman Sachs estimate that by the end of the decade, global dominance will be led by three countries: China, India, and the United States, which together will account for more than 50% of global GDP. On this same trajectory, Europe could represent less than 10% of global GDP by 2050 if no changes are made to alter its current path.

Europe is not only beset by bureaucracy or a lack of sovereignty in certain areas, but also by fundamental issues such as an aging population. It is estimated that by 2030 the labor force will be 2% smaller than it is today, and those over 65 will account for more than 44% of the population.

Against this backdrop, Europe faces far-reaching challenges that will define its global presence and role in the years ahead. However, challenges and crises also bring opportunities. If the Old Continent can address them, it could unlock significant potential for its economies. Unlike other regions, Europe is home to some of the world’s leading companies in sectors such as textiles, food, energy, and, of course, luxury.

The European capital market

European companies, which receive far fewer headlines than their American counterparts, are essential in sectors such as luxury goods, precision industrial machinery, and the chemical industry. In addition, at the start of 2026, companies were trading at 13 times earnings compared with 22 times for companies in the S&P 500, indicating more attractive valuations.

And not only that: in terms of dividend yield, those in the Old Continent significantly outperform their US counterparts (3.5% versus 1.5%). Adding to this are more than €33 trillion in household financial savings, part of which is expected to be channeled into financing European companies through the ongoing work on the European Savings and Investment Union.