North American countries are redefining their role in an increasingly fragmented world where the trend toward offshoring production coexists with the uncertainty stemming from U.S. policy, cementing Mexico and Canada as key partners, while the United States seeks to maintain its global leadership in a less predictable environment.

One of the most frequently repeated mantras at conferences, events, and in economic analyses is that we are likely heading toward a world that is fragmented into new blocs and less globalized. The main protagonist of these blocs remains in the North American region, with the United States trying to maintain its global leadership.

Although North America includes the United States, Canada, and Mexico, it is the former that attracts all the attention. But, to understand the current situation, it is necessary to contextualize it, understanding past scenarios. After the first term of Donald Trump (2017-2021) and the global Covid-19 pandemic, the world changed. The United States implemented a tariff policy that has pushed these rates to their highest level since the 1940s and accelerated the trend known as nearshoring.

Canada and Mexico, meanwhile, are operating under the threat of new tariffs and the need for the United States to bring production closer to its territory to reduce risks in supply chains. A continued clash between threats from the US president and the search for other trading partners.

The situation in North America in 2026: a change in their role in the world

“The region’s current situation hinges on Trump’s policy decisions, which ‘are calling into question the very foundations that they themselves established after the end of World War II,’” says Pedro del Pozo, director of financial investments at Mutualidad. This expert claims that the U.S. has decided to change a leadership model that benefited it for a much more self-centered, less global concept, in which American strength remains dominant but which, at its core, “consists of positioning the U.S. not as a leading nation, but as a primus inter pares in a more fragmented world.”

These measures have fueled the “Sell America” sentiment at the start of the year, compounded by certain economic issues that are causing growing concern, such as high levels of debt. Some “cons” are reinforced by some “pros”, such as robust growth, the strength of its companies and the opportunity to dominate the new world marked by the expansion of artificial intelligence (AI).

We must not forget that, in this analysis of the present, the United States “has cutting-edge technology, the world’s reserve currency, the most developed financial system, and a powerful and highly dynamic domestic economy.” Furthermore, they have the greatest capacity for global influence that exists today, both through their economy and their military strength. But above all, they have credibility in their system,” adds the director of financial investments at Mutualidad.

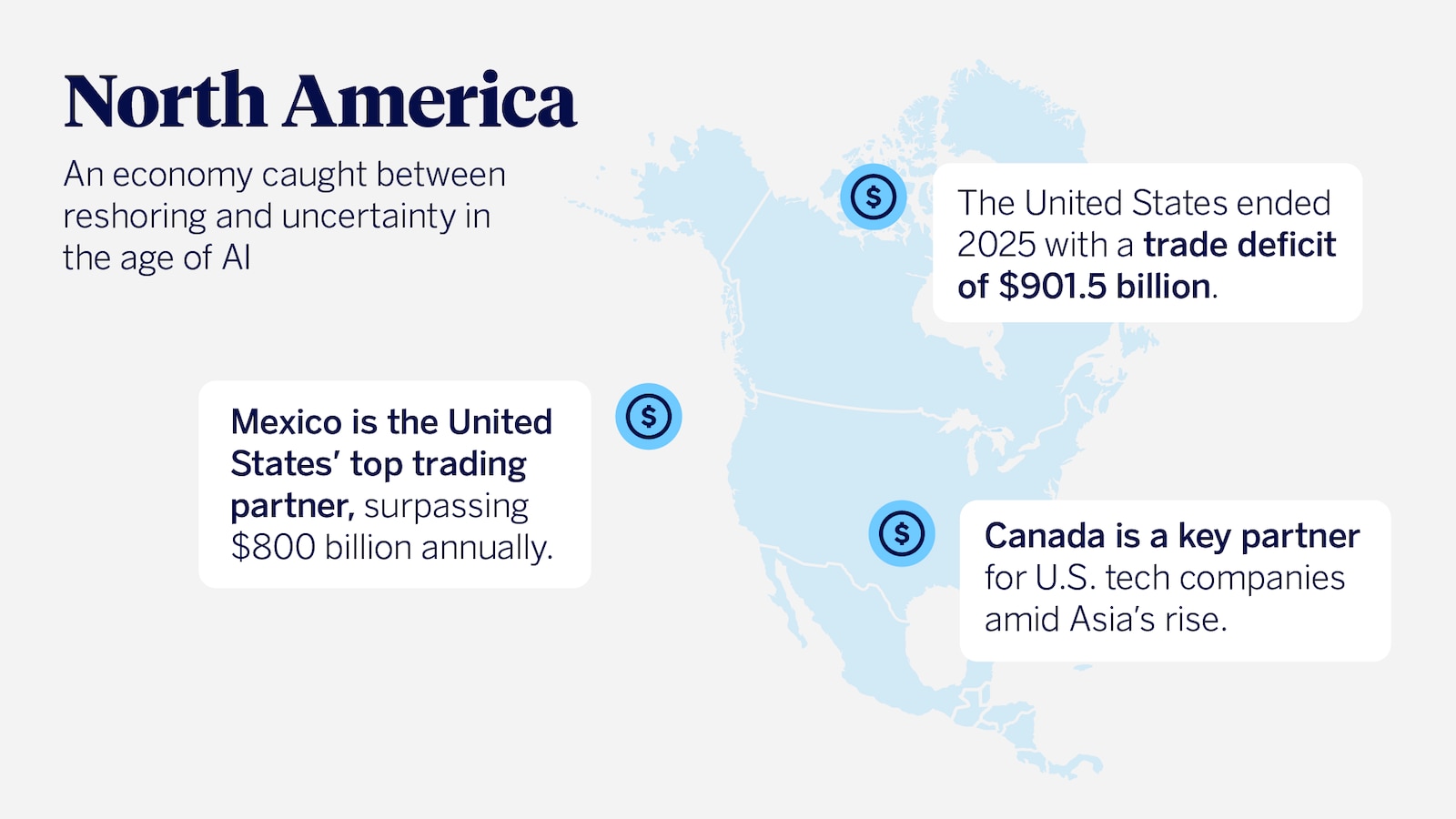

Its northern and southern neighbors, Mexico and Canada, are presented as indispensable partners. Mexico has consolidated its position as the United States' top trading partner, exceeding $800 billion in annual trade; figures driven by the American giant's need for nearshoring. Sectors such as automotive and manufacturing have continued to grow. Thus, the United States ended 2025 with a trade deficit of $901.5 billion, just below the $903 billion recorded the previous year. Total imports reached a record high of $4.334 trillion, representing a 5% increase over the previous year, while exports totaled $3.432 trillion, with an annual growth of 6%.

To the north, Canada continues to position itself as the great storehouse of critical resources. In fact, Ottawa is a key partner for American technology companies to reduce their exposure to Asian rare earth elements, which are so coveted and protected by China. Although both countries continue to face risks stemming from the current White House’s unpredictable policies and the review of the USMCA.

Risks that threaten the global financial system

The risks facing the United States are not minor, neither in their severity nor in their implications and impact on the global economy. The much-discussed de-dollarization, coupled with high public debt, are the two big elephants in the room. “Although the main risk, of course, is that credibility will be undermined—something that has undoubtedly been happening to some extent in recent months," warns Pedro del Pozo.

According to the expert, “if the U.S. ceases to be reliable, international investors will not buy their debt, and their chronic deficits will no longer be possible.” And that's not all: If the use of the dollar as the primary currency in international trade is threatened, “the U.S. economy will be affected.” Therefore, these appear to be the main areas that should be given attention at present and in future developments.

The goal from now on is to continue leading

At this point, we know where the region has come from (business restructuring and nearshoring), what its current state is (growth and risks), and it remains to be seen what the future holds. A future in which AI and technology play a leading role. In the near and medium future, the world faces a new technological revolution involving several factors: companies, minerals, energy and labor impact.

From the end of 2025, investors are concerned about the large amount of spending on AI, but also about its impact on the economy. Understanding what will happen in the labor market, how companies will be able to monetize all their current investments, and the necessary physical capacity (materials and energy) are challenges facing North America and the world.

To better understand this challenge, it is worth noting that big tech companies spend around $200 billion annually on data center investments; the electricity demand of data centers will double in the United States by 2030, reaching 9% of total demand compared to the current 4% (with Canada as a key player in meeting that demand); these infrastructures require three times more copper and more complex cooling systems; finally, according to the IMF, AI could automate up to 25% of work tasks.

All of the above will have a very strong impact on American GDP. According to estimates by consulting firms such as PwC and Goldman Sachs, AI could add up to $15.7 trillion to the global economy, and of that amount, the United States could capture between 14% and 21% of its cumulative GDP over the next decade. Therefore, leading this race will be what keeps them at the top of the world rankings.

Del Pozo believes that, to the extent that the U.S. strays from this path, its power will become just one among the new blocs that are taking shape. “China, without a doubt, whose long-term vision makes it a likely candidate to take over from a United States that is weaker and more alone. But a more united European bloc could also serve as a political and economic counterweight rather than the loyal ally it has been during the Cold War and the period following the collapse of the Soviet Union. Flawed US leadership will inevitably lead to its decline," he points out. Faced with this situation, the U.S. has just recently launched the "Vault Project", a $12 billion strategic reserve for critical minerals, where Canada is the main supplier to replace the 80% dependence on China for rare earths.

Canada, the energy supplier the U.S. needs.

Big tech companies are not only competing to lead the new global AI landscape, but also to secure resources. These resources include not only chips and various hardware, but also energy. These companies signed the Rate Payer Protection Pledge to ensure that they would finance their own energy infrastructure and not drive up energy bills for American households. This is where Canada is coming into play because it is cheaper to import Canadian energy than to build new plants. In fact, the New England Clean Energy Connect, which links Quebec with Massachusetts, was already commissioned in January of this year.

Despite these challenges, the structural foundations of the US economy, from institutional strength to the central role of the dollar, continue to underpin its position as the main global benchmark.